A business can look busy on the outside and still be losing money behind the counter. That is why Break Even Sales Volume matters before you hire, discount, rent a larger space, buy inventory, or add another service package. It tells you the sales level where revenue covers your fixed and variable costs, with no profit yet and no loss left to absorb. For a U.S. service firm, that might mean the number of monthly client retainers needed to cover payroll, software, insurance, and office costs. For a product business, it might mean the number of candles, shirts, meal kits, or machine parts needed to cover rent, materials, packaging, and labor. Owners who track this early make calmer decisions. They price with intent, not panic. A resource like business growth visibility can support the wider marketing side, but the math still has to work inside the business first. Sales are exciting. Safe sales are better.

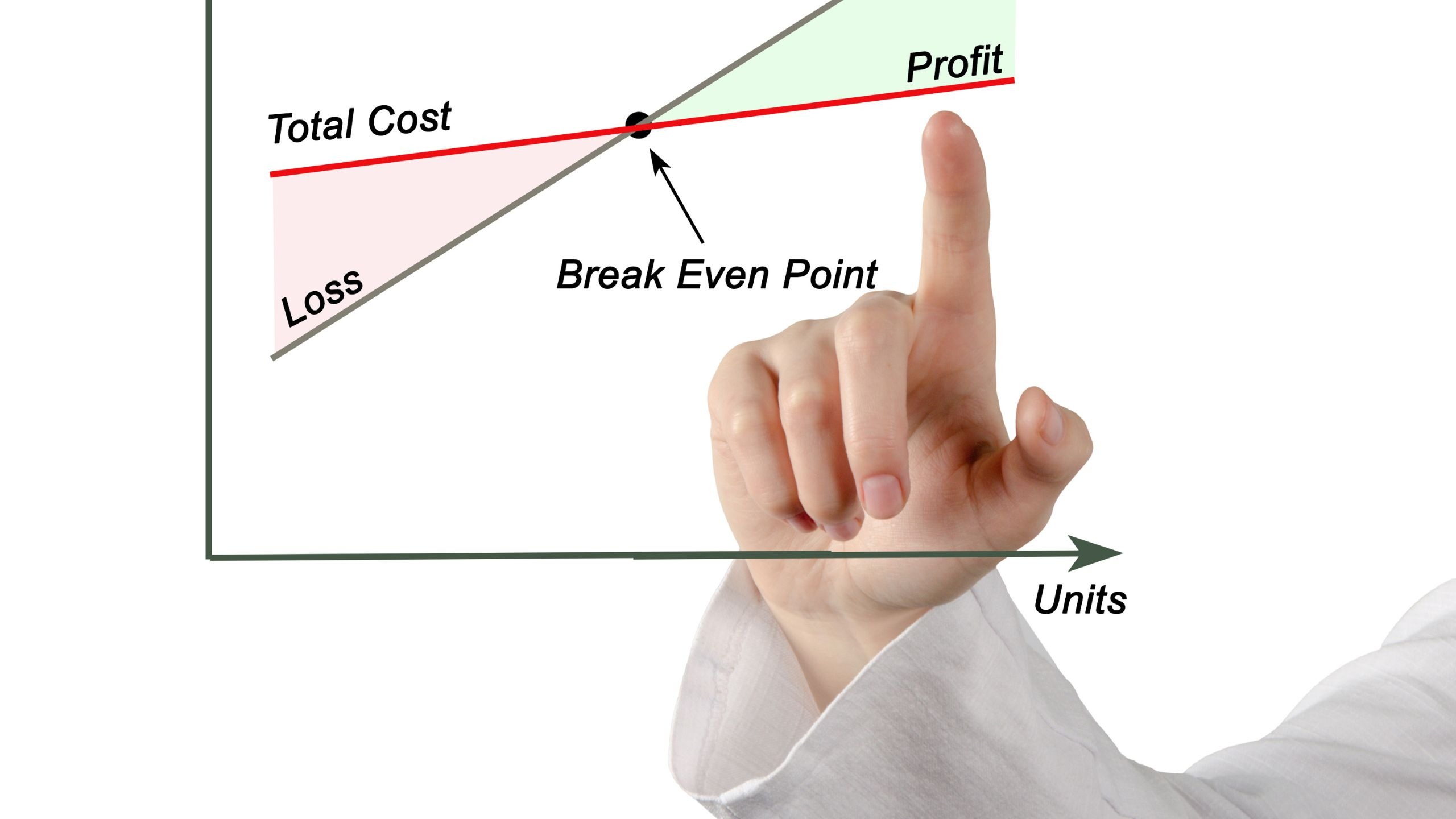

Why the Break-Even Point Gives Owners a Cleaner View of Risk

The break-even point is not a fancy finance exercise. It is the line between guessing and knowing. Many small business owners in the USA judge health by bank balance, daily orders, or how full the calendar looks. Those signs help, but they can fool you. A packed week with thin margins can lose more money than a slower week with better pricing.

Why Revenue Alone Can Mislead You

Revenue feels good because it is visible. A bakery rings up $18,000 in a month, and the owner feels momentum. Then flour, butter, boxes, payroll taxes, rent, payment fees, repairs, and waste take their bites. By the end, the “good month” may be closer to survival than success.

That is the first hard lesson. Sales volume without cost context is noise. A local cleaning company can add ten new clients and still weaken its position if travel time, supplies, and labor hours rise faster than the invoice total.

The break-even point fixes that blind spot by tying sales to fixed and variable costs. Fixed costs are the bills that show up even when sales are slow. Variable costs move with each job or unit sold. Once you separate them, the business stops looking like one large pile of money and starts looking like a machine with parts you can adjust.

What Owners Learn Before They Spend More

The best use of break-even thinking is before a big move, not after. Say a Dallas mobile detailing service wants to lease a small shop. The rent is $2,400 a month, utilities may add $600, and insurance goes up by $300. That is $3,300 in new fixed cost before one extra car is cleaned.

If the average job brings in $90 after direct supplies and labor, the owner needs about 37 more jobs each month to cover the new shop. That changes the question. It is no longer, “Can we afford the rent?” It becomes, “Can we bring in 37 profitable jobs every month without burning out the team?”

Here is the non-obvious part: a higher fixed cost is not always bad. It can be smart when it lowers variable costs or raises the price you can charge. The shop may cut travel time, improve scheduling, and make premium packages easier to sell. The math helps you see whether the trade is worth it.

Break Even Sales Volume Formula and the Numbers You Need First

Break Even Sales Volume is easier than many owners expect, but only when the inputs are honest. The formula for units is fixed costs divided by contribution margin per unit. The formula for sales dollars is fixed costs divided by contribution margin ratio. Those two versions serve different businesses, and using the wrong one can create false confidence.

How to Separate Fixed and Variable Costs Without Overthinking It

Start with fixed costs. These are monthly costs that stay in place across normal sales levels. Rent, full-time salaries, insurance, website hosting, loan payments, bookkeeping, and core software often belong here. They do not disappear because one customer cancels.

Then list variable costs. These are tied to each sale. A product seller may count materials, packaging, shipping labels, marketplace fees, and piece-rate labor. A service business may count contractor hours, mileage, job supplies, payment processing fees, and sales commissions.

Some costs sit in the middle. A gym may have a base electric bill, then higher costs when classes fill up. A catering company may have salaried kitchen staff plus extra event labor. Do not force every cost into a perfect box. Split mixed costs with a fair estimate and update it once real numbers arrive.

How Contribution Margin Turns Sales Into Useful Math

Contribution margin is the money left from each sale after variable costs. If a Los Angeles candle brand sells a candle for $30 and spends $11 on wax, fragrance, jar, label, box, and transaction fees, the contribution margin is $19.

If monthly fixed costs are $7,600, the owner divides $7,600 by $19. The result is 400 candles. That is the break-even point in units. Sell fewer, and the business loses money. Sell more, and each extra candle helps profit, assuming costs stay in range.

For services, the same logic applies. A Phoenix bookkeeping firm charges $500 per monthly client. Direct contractor help and software tied to that client cost $140. The contribution margin is $360. If fixed costs are $9,000, the firm needs 25 clients to cover costs.

The counterintuitive part is that price increases can beat sales increases. Raising the bookkeeping package from $500 to $550 may do more than chasing five more clients, especially if the same team can serve the current client base well. More sales are not always the cleanest path. Better-margin sales often win.

Applying the Math Differently in Service and Product Businesses

Service and product businesses share the same break-even logic, but they do not feel the same in daily operations. A service business is usually limited by time, skill, and staff capacity. A product business is often limited by inventory, production, cash tied up in stock, and fulfillment. The formula stays simple. The judgment around it does not.

Service Businesses Must Price Around Time Capacity

A service owner cannot only ask, “How many clients do I need?” The sharper question is, “Do I have enough billable hours to serve them without wrecking quality?” A Chicago web design studio may need eight projects a month to break even on paper. That means nothing if the team can finish only five good projects without late nights and rushed work.

This is where small business pricing strategy connects to the math. If a designer charges $2,500 per site and direct contractor costs are $700, the contribution margin is $1,800. With $14,400 in fixed costs, eight projects cover the month. But if each site takes 55 hours, eight projects require 440 production hours. The sales target may be possible in dollars and impossible in time.

That is why service firms often need packages, retainers, or minimum fees. A clear monthly package can protect margin and reduce unpaid admin time. A plumber, marketing consultant, lawn care company, or tax preparer all face the same issue: the calendar is a cost center when it is filled with low-margin work.

Product Businesses Must Watch Cash Before Profit Appears

Product sellers have another trap. They may hit the break-even point on paper while cash is still tight. Inventory has to be bought before it is sold. Shipping supplies have to be stocked. Returns may arrive weeks after a sale. A small apparel brand in North Carolina may need to sell 1,200 shirts to cover costs, but it may need to order 1,500 shirts upfront to meet size and color demand.

That creates risk before the first sale lands. Product owners should run the break-even point twice: once for profit and once for cash timing. The profit version asks, “How many units cover total costs?” The cash version asks, “How much money leaves before customers pay us?”

Here is the less obvious insight: a product with a lower margin can still be safer if it turns faster and has fewer returns. A $70 item with a $30 contribution margin looks strong. But if it sits for six months, needs heavy discounting, and comes back often, the math gets dirty. A $25 refill item with a $10 margin may build a steadier business because customers buy it again and inventory moves.

Using Break-Even Results to Make Better Pricing, Hiring, and Growth Decisions

Once you know your break-even point, do not leave it in a spreadsheet. Use it as a decision filter. Every new hire, discount, location, ad campaign, subscription, or product line should answer one question: how does this change the sales needed to stay safe?

When Discounts Hurt More Than They Help

Discounts can raise orders and still damage the business. A Miami meal prep company selling weekly plans for $120 may spend $72 on food, containers, kitchen labor, and delivery. That leaves a $48 contribution margin. If the company offers 20% off, the price drops to $96. If variable costs stay $72, the contribution margin falls to $24.

That discount cuts the margin in half. Now the company must sell twice as many plans to create the same contribution toward fixed costs. Many owners miss that because order count rises and the kitchen feels busier.

A better move may be a bonus item with low variable cost, a prepaid plan, or a referral credit after the new customer stays for one full billing cycle. This is where cash flow planning for owners belongs in the same conversation as break-even math. Discounts should be designed around margin, not hope.

When Hiring or Expansion Changes the Sales Floor

Hiring creates relief, but it also raises the break-even point. Suppose an Atlanta HVAC company adds a dispatcher at $4,500 per month including payroll taxes and benefits. If the company earns a $300 contribution margin per completed service call, it needs 15 extra completed calls per month to cover that role.

That may be a smart hire if the dispatcher reduces missed calls, improves scheduling, and helps technicians complete more paid work. It may be a poor hire if the phone is not ringing enough yet. Break-even thinking does not say yes or no by itself. It shows the size of the promise the business must keep.

Expansion works the same way. A second location, new truck, added software, larger warehouse, or ad contract all raise the fixed cost base. The owner should translate each one into sales volume. “This tool costs $900 a month” is vague. “This tool needs three extra jobs a month to pay for itself” is clearer.

The counterintuitive move is to use break-even math even when you can afford the expense. Cash in the bank can hide weak decisions. A business with savings can carry bad costs for months before the damage becomes clear.

Conclusion

A company gets stronger when the owner knows the floor beneath their feet. Sales goals matter, but they should never float away from cost structure, capacity, and margin. The Break Even Sales Volume gives you that floor in plain language. It tells a service owner how many clients, projects, appointments, or billable hours must be sold before profit begins. It tells a product owner how many units or sales dollars must move before fixed costs are covered. Better yet, it exposes the hidden trade-offs behind pricing, hiring, discounts, and expansion. You do not need a large finance team to use it. You need honest costs, a steady review habit, and the nerve to change prices or plans when the numbers say the model is too thin. Before the next big push, run the math once with your current setup and once with the change you want to make. Then build from the version that can survive real life.

Frequently Asked Questions

How do you calculate break-even sales for a small business?

Use fixed costs divided by contribution margin. For units, subtract variable cost per sale from the selling price, then divide fixed costs by that number. For sales dollars, divide fixed costs by the contribution margin ratio.

What costs should be included in a break-even calculation?

Include fixed costs such as rent, salaries, insurance, software, loan payments, and core admin expenses. Add variable costs tied to each sale, such as materials, labor, packaging, shipping, commissions, supplies, and payment processing fees.

Is break-even different for service businesses and product businesses?

The formula is the same, but the pressure points differ. Service businesses must watch labor hours and capacity. Product businesses must watch inventory, production costs, returns, and cash tied up before items are sold.

What is a good break-even point for a new business?

A good break-even point is one the business can reach with realistic sales, healthy pricing, and enough capacity to serve customers well. If the target requires constant discounts, unpaid labor, or perfect demand, the model may need adjustment.

How often should a business update its break-even numbers?

Review it monthly during the first year or whenever prices, rent, payroll, supplier costs, or sales mix changes. Mature businesses can review quarterly, but fast-moving companies should check more often because small cost shifts can change the target.

Can a business be profitable before reaching break-even?

No, not under the full break-even model. Before that point, revenue has not covered total fixed and variable costs. A single sale may have a positive contribution margin, but the whole business still needs enough sales to cover fixed costs.

Why does contribution margin matter more than revenue?

Revenue shows how much money comes in. Contribution margin shows how much is left after direct costs to cover fixed costs and profit. A business with lower revenue but stronger margins can be healthier than a busier one with weak margins.

What happens if variable costs increase after I calculate break-even?

The break-even point rises because each sale contributes less toward fixed costs. Recalculate with the new cost, then decide whether to raise prices, reduce waste, change suppliers, adjust packaging, or drop low-margin offers.